Structural Context

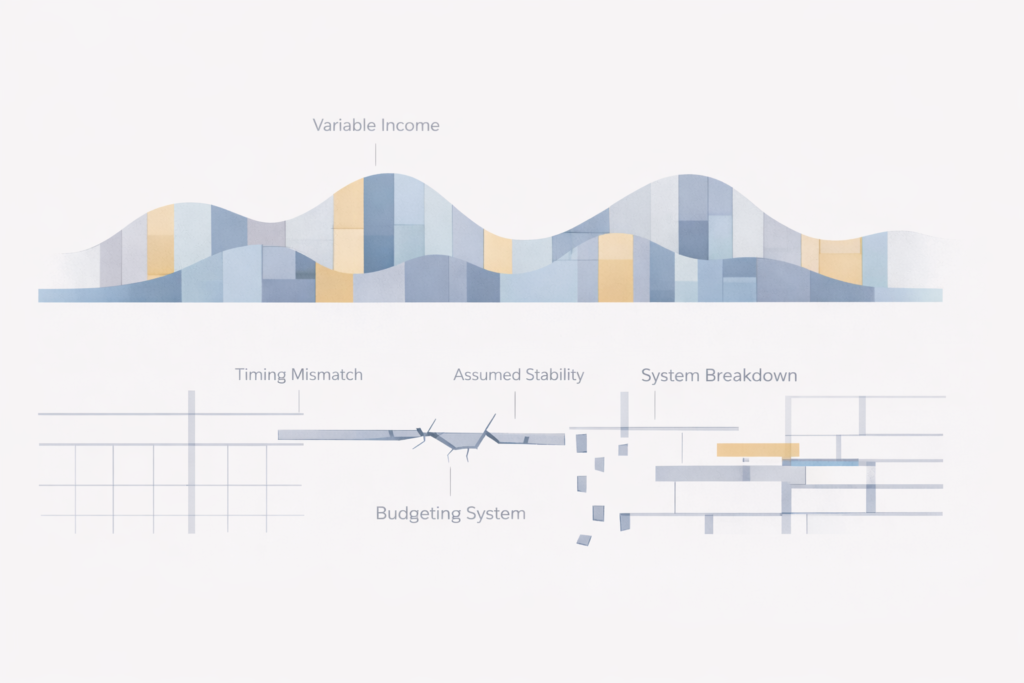

Why budgeting breaks down under variable income conditions becomes evident when income timing disperses across irregular payout cycles. Calendar-based controls assume synchronized inflows and expenses. When that alignment fractures, budgeting appears unstable even if total earnings remain consistent.

This explains why income feels unpredictable even when total revenue does not materially change.

Quick Answer

Traditional budgeting assumes predictable income timing and stable monthly inflows.

Freelance income systems operate with variable payout timing and uneven distribution.

When timing fluctuates, calendar-based allocation loses synchronization. The breakdown is structural — not behavioral.

Why This Happens for Freelancers

Budgeting models were designed for payroll systems:

• Fixed pay dates

• Known inflow amounts

• Stable intervals

Freelance systems operate differently:

• Irregular invoice approvals

• Client-controlled payout schedules

• Payment clustering

• Timing gaps between earning and access

As established in the analysis of cashflow timing risk, income may exist while remaining inaccessible. Budgeting assumes earning and accessibility occur within the same monthly frame. Freelance systems separate them.

What Budgeting Assumes

Budgeting rests on three assumptions:

1. Income Arrives on Schedule

Allocation is based on known dates.

2. Monthly Inflows Are Stable

Spending categories reflect expected consistency.

3. Income and Expenses Share a Calendar Rhythm

Cash enters and exits within aligned cycles.

These assumptions allow budgeting to function as a balancing mechanism. When any collapse, synchronization fails.

How Variable Timing Disrupts Monthly Allocation

Budgeting is calendar-based.

Freelance income is event-based.

When a payment shifts by two weeks:

• One month appears underfunded

• The next appears inflated

• Allocation decisions distort

Total revenue may be unchanged; only the arrival window shifts.

Budgeting interprets timing variance as overspending or planning failure. It is temporal misalignment.

Expense Matching Under Income Dispersion

Most expenses operate on fixed schedules:

• Rent

• Utilities

• Software subscriptions

• Insurance

These obligations do not adjust to income timing.

When income arrives unpredictably, expenses remain rigid while inflows shift, creating temporary liquidity compression.

Budgeting does not distinguish between structural compression and excess spending. It registers both as category failure.

Surplus Expectations and Illusory Stability

Budgeting assumes surplus reflects discipline.

Under variable timing, surplus may reflect clustering.

• Categories appear overfunded

• Surplus expands

• The system feels stable

If a gap follows:

• Categories contract

• Shortfall appears

• Instability is inferred

The annual pattern may be consistent; the monthly frame misrepresents it.

Budgeting interprets timing dispersion as behavioral volatility. The system is responding to structure.

Why “Budget Failure” Is Not Financial Irresponsibility

When budgeting breaks down, individuals internalize failure.

Control systems fail when environmental assumptions are violated.

If a model requires predictable timing and the environment does not provide it, the control cannot stabilize outcomes.

This is not a discipline gap.

It is a model–environment mismatch.

Freelancers operating under volatility are not less responsible. They are operating inside a structure for which traditional budgeting was not engineered.

How This Fits Inside the FM Mastery System

This analysis sits within the AI-Powered Money Management pillar of FM Mastery, where financial instability is examined as system behavior rather than personal failure.

Final Thought

When a control mechanism fails repeatedly under stable effort, the question is structural alignment.

Budgeting is calibrated for predictable inflows. Variable-timing income systems operate under dispersion.

Recognizing this removes confusion. It restores authority to the operator and clarifies that the instability observed is mechanical — not personal.