RISK MISINTERPRETATION — Income Variability vs Income Risk in Freelance Systems addresses one of the most common structural misunderstandings in freelance finance: confusing income variability with income risk. For freelancers operating under irregular income conditions, volatility is normal — but structural fragility is not. Understanding the difference between income variability and income risk is essential for building a durable financial system that can function under uncertainty.

Freelancers often describe their income as “risky.”

What they usually mean is that it moves.

Monthly totals change. Payment timing shifts. Large invoices cluster, then disappear. Cashflow rarely follows a straight line.

Movement is not danger.

The most persistent financial misjudgment in freelancing is conflating income variability with income risk. When treated as identical, decision logic degrades. Buffers are oversized without structural improvement. Volatility is fought instead of understood. Stability is pursued visually rather than architecturally.

This distinction matters because freelance income is naturally variable — not automatically fragile.

This approach is part of a broader AI financial system for freelancers designed to manage financial decisions under income uncertainty.

Quick Answer

Income variability is the normal fluctuation of freelance earnings over time.

Income risk is structural exposure that threatens long-term stability.

Volatility describes movement.

Risk describes fragility.

Confusing them leads to defensive decisions that do not improve durability.

Why This Happens for Freelancers

Freelancers operate without payroll smoothing.

Traditional employment compresses income into predictable intervals. Freelance systems distribute revenue unevenly. Projects begin and end. Retainers renew or lapse. Clients delay payment. Workloads spike and contract.

This creates amplitude shifts — larger and smaller revenue months — even when annual income remains stable.

Visually, this resembles instability.

Behaviorally, irregularity triggers caution. Humans interpret unpredictability as threat. When income moves, the instinct is to label movement itself as danger.

Volatility alone does not indicate structural weakness.

A bridge can sway without collapsing. A market can fluctuate without failing. A freelance income stream can oscillate without being unsafe.

The error begins when surface movement is interpreted as structural fragility.

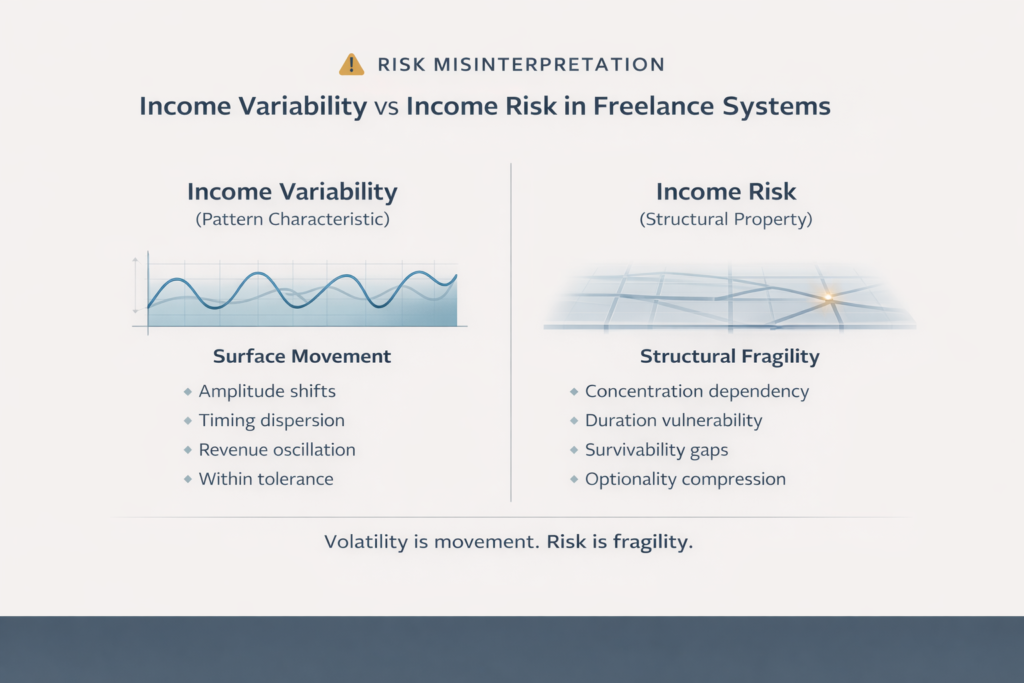

Defining Income Variability (Surface Movement)

Income variability is a pattern characteristic.

It describes:

• Amplitude shifts in monthly revenue

• Timing dispersion of payments

• Project clustering

• Seasonal oscillation

• Client cycle fluctuations

These shifts occur even in structurally strong systems, including those affected by Cashflow Timing Risk in Freelance Systems.

Variability answers: “How much does income move?”

It does not answer: “Will the system survive?”

A freelance system can show wide variance yet remain durable if revenue sources are diversified, client relationships recurring, expenses proportional, and cashflow gaps absorbable.

In this context, volatility operates within tolerance.

Movement is visible. Resilience is not.

This is why variability is misdiagnosed as instability — it is observable; structural strength is abstract.

Defining Income Risk (Structural Fragility)

Income risk is a structural property.

It refers to exposure that threatens continuity.

Risk exists when the income system cannot withstand disruption. Its indicators are architectural, not visual.

Structural income risk includes:

• Concentration dependency — over-reliance on a single client or revenue source

• Duration vulnerability — limited survivability during income gaps

• Cashflow survivability gaps — obligations that outlast revenue

• Optionality compression — inability to decline work without destabilization

• Capacity fragility — income tied to unsustainable workload

Unlike variability, risk does not require visible volatility.

Smooth monthly income can carry high structural risk if it depends on one fragile contract.

Uneven months can coexist with low risk if income sources are distributed and obligations controlled.

Risk answers: “What happens if disruption occurs?”

Variability answers: “How uneven is the pattern?”

They are not interchangeable.

Why Freelancers Confuse the Two

1. Visual Bias

Financial dashboards display fluctuation, not resilience. Movement appears alarming. Structural strength remains hidden.

Humans overweight what they can see.

2. Employment Anchoring

Most freelancers were conditioned under fixed-salary systems. Stability meant identical pay intervals. Deviation feels abnormal, even when structurally sound.

3. Emotional Encoding

Income inconsistency creates discomfort. That discomfort is labeled “risk,” even when no structural exposure exists.

The result is conceptual drift: volatility becomes danger; danger becomes fluctuation.

System-Level Consequences of Misinterpretation

1. Overfunding Surface Protection

Freelancers attempt to neutralize visible volatility. Large buffers are built to eliminate discomfort, not structural weakness.

Surface calm replaces systemic strength.

2. Underbuilding Structural Durability

Focus on fluctuation leaves deeper exposures untouched:

• Revenue concentration

• Contract fragility

• Duration mismatches

• Cost rigidity

The system appears defended yet remains vulnerable.

3. Reactive Financial Behavior

Each low-income month is treated as crisis. Each high-income month as recovery.

Decision-making becomes cyclical rather than strategic.

Attempting to eliminate variability increases instability by preventing structural improvement.

Preparing the Ground: Rethinking Emergency Logic

Emergency frameworks often assume volatility equals danger.

In freelance systems, volatility is baseline.

The relevant question is not: “How do I eliminate income fluctuation?”

It is: “Does my structure survive fluctuation?”

Emergency thinking focused on smoothing income ignores durability mechanics, which is why Why Emergency Funds Misalign With Irregular Income requires structural reconsideration.

If variability is expected, resilience must be engineered into the system — not imposed on the pattern.

The objective is survivability under oscillation, not elimination of oscillation.

Practical Takeaways

• Volatility is observable movement. Risk is structural exposure.

• Uneven income does not signal fragility.

• Smooth income can conceal dependency risk.

• Defensive responses to fluctuation may ignore structural weakness.

• Stability is measured by survivability, not visual uniformity.

Who This Applies To

This applies to freelancers who:

• Experience monthly revenue swings

• Feel anxiety despite stable annual income

• Build large reserves yet feel exposed

• Have smooth income but rely heavily on one client

It does not apply to individuals whose instability results from declining demand rather than structural design.

Final Thought

Stability is not the absence of movement.

It is the presence of structure.

Freelance income is naturally variable. That variability is not a defect. It is a pattern characteristic of project-based work.

Risk emerges when architecture cannot withstand disruption.

When volatility is treated as the enemy, fragility remains invisible.

When structure becomes the focus, volatility becomes tolerable.

Income variability is a visual phenomenon.

Income risk is a structural reality.

Understanding the difference is the beginning of financial clarity.