How Freelancers Budget With Irregular Income (System-Based)

Budget irregular income freelancers using a system-based approach that controls income timing, allocation flow, and weekly decision-making instead of fixed monthly budgeting.

Budgeting with irregular income for freelancers fails when using traditional monthly methods because income timing is unpredictable. The solution is a system-based approach that stabilizes financial decisions using income floors, weekly control cycles, behavioral allocation, and timing-aware cashflow management.

Freelancers do not need better budgeting discipline. They need a system that works under volatility.

Most freelancers believe they struggle with budgeting because they lack discipline.

This assumption is incorrect.

Freelancers do not fail because they cannot manage money.

They fail because they are using a system that was never designed for how their income works.

Traditional budgeting assumes a controlled financial environment:

- income arrives on predictable dates

- monthly earnings are stable

- expenses align with income cycles

Freelance income breaks all of these assumptions.

Income becomes:

- irregular in timing

- uneven in distribution

- dependent on external factors like clients and approvals

This creates a condition where:

👉 financial decisions must be made under uncertainty

Budgeting was not designed for uncertainty.

It was designed for predictability.

That is why it fails.

And that is why freelancers repeatedly feel like they are doing something wrong — even when they are consistent.

To effectively budget irregular income freelancers, the approach must shift from monthly planning to system-based control aligned with income volatility.

System Identity: Budgeting vs Financial Control System

This is not a budgeting method.

This is not a tracking tool.

This is not financial advice.

This is a financial control system designed specifically for freelancers with irregular income.

Traditional budgeting focuses on planning spending.

This system focuses on controlling decisions.

The difference is fundamental.

Budgeting Approach

- predict income

- allocate categories monthly

- adjust when things go wrong

System-Based Approach

- accept income unpredictability

- control allocation timing

- stabilize decisions regardless of income

Budgeting assumes stability and tries to enforce discipline.

This system assumes volatility and enforces structure.

This is why one fails and the other works.

Freelancers do not need better budgeting tools.

They need a system that aligns with their financial reality.

To effectively budget irregular income freelancers, the approach must shift from monthly planning to system-based control aligned with income volatility.

Why Freelancers Struggle With Budgeting (Behavioral Reality)

Financial instability is not only structural. It is behavioral.

Freelancers operate in environments that create continuous cognitive pressure:

- uncertain income timing

- client dependency

- inconsistent workload

- lack of predictable safety nets

This environment produces predictable behavioral patterns:

1. Overspending During High-Income Periods

When income spikes, freelancers experience relief and optimism. Spending increases because stability feels temporary.

2. Restriction During Low-Income Periods

When income drops, decisions become defensive. Spending is cut aggressively, often irrationally.

3. Avoidance Under Uncertainty

When future income is unclear, decision-making slows or stops. This leads to delayed planning and reactive choices.

Traditional budgeting ignores these patterns.

It assumes consistent behavior under consistent conditions.

Freelancers do not operate under consistent conditions.

This system integrates behavioral reality into financial control.

It does not fight behavior.

It structures it.

Why Budgeting Fails for Freelancers With Irregular Income

Budgeting is supposed to create financial stability.

For freelancers, it often creates the opposite.

You follow a budget during a strong income period, and everything appears under control.

Then income slows, payments delay, or work becomes inconsistent — and the system collapses.

This creates a repeating cycle:

- confidence during high-income periods

- restriction during low-income periods

- uncertainty across both

Over time, budgeting stops feeling like a solution.

It starts feeling like a constraint that only works temporarily.

This leads to a deeper problem:

👉 freelancers begin to lose trust in their own financial decisions

They assume the issue is:

- lack of discipline

- poor planning

- inconsistent tracking

But these are symptoms, not causes.

The real issue is that budgeting operates on assumptions that do not apply to freelance income.

Budgeting expects stability.

Freelance income is defined by variability.

When a system designed for stability is applied to variability, failure is inevitable.

The challenge to budget irregular income freelancers is not about spending control, but about timing mismatch between income and expenses.

The Real Root Cause: Income Timing Mismatch

The core problem is not how much freelancers earn.

It is when income becomes available.

Freelance income operates in a fundamentally different structure compared to salaried income.

Freelance Income Characteristics

- payments depend on client approval cycles

- projects complete at irregular intervals

- invoices are paid with delays or inconsistencies

- multiple income sources create uneven inflow patterns

This creates what can be defined as income dispersion.

Income is not absent — it is distributed unpredictably across time.

Expense Characteristics

- rent and housing follow fixed monthly schedules

- subscriptions renew on fixed dates

- living costs remain consistent regardless of income timing

This creates a structural mismatch:

Income is variable and event-based

Expenses are fixed and calendar-based

Budgeting assumes these two systems are aligned.

They are not.

This misalignment produces what freelancers experience as:

- temporary cash shortages despite sufficient annual income

- false surplus during clustered payment periods

- difficulty making forward-looking financial decisions

Budgeting does not distinguish between:

- structural timing gaps

- actual overspending

It treats both as failure.

This leads freelancers to misdiagnose the problem.

They try to fix behavior when the issue is structural.

Why Traditional Budgeting Can Never Work for Irregular Income

Most financial advice suggests improving budgeting techniques.

This is fundamentally flawed.

The problem is not how budgeting is used.

The problem is what budgeting assumes.

Assumption 1: Income Timing is Predictable

Budgeting requires knowing when money will arrive.

Freelancers cannot control this.

Therefore, allocation decisions are always based on uncertainty.

Assumption 2: Monthly Cycles Represent Reality

Budgeting compresses financial activity into monthly windows.

Freelance income does not follow monthly cycles.

It follows project timelines and client behavior.

Assumption 3: Discipline Can Compensate for Variability

Budgeting assumes consistency in behavior.

Freelancers operate under fluctuating stress, income, and workload.

Behavior cannot remain constant under changing conditions.

These assumptions create unavoidable breakdown points.

No variation of budgeting can resolve them.

This includes:

- 50/30/20 budgeting

- zero-based budgeting

- envelope systems

- app-based budgeting tools

All of these methods depend on predictable income timing.

Freelancers do not have predictable income timing.

Therefore, all of these methods fail at scale.

This is not a matter of optimization.

This is a matter of compatibility.

Budgeting is not designed for irregular income.

It cannot be adapted to it.

It must be replaced.

The Shift: From Budgeting to System-Based Financial Control

Once the structural problem is clear, the solution becomes obvious.

Freelancers do not need to improve budgeting.

They need to replace it with a system that works under volatility.

This requires a shift in thinking:

- from predicting income → to responding to income

- from monthly planning → to continuous control

- from discipline → to structure

Instead of asking:

“How do I budget better?”

The correct question becomes:

👉 “How do I stabilize financial decisions when income is unpredictable?”

The answer is not a method.

It is a system.

That system is defined in the next section.

The Irregular Income Budgeting System (System That Replaces Budgeting)

This system exists because traditional budgeting cannot operate under income volatility.

It is not an improvement of budgeting.

It is a replacement.

Instead of attempting to predict income and allocate in advance, this system stabilizes financial decisions regardless of when income arrives.

This is the defining shift:

Control replaces prediction.

Structure replaces discipline.

Stability is engineered, not assumed.

This system is specifically designed to help budget irregular income freelancers without relying on predictable monthly income.

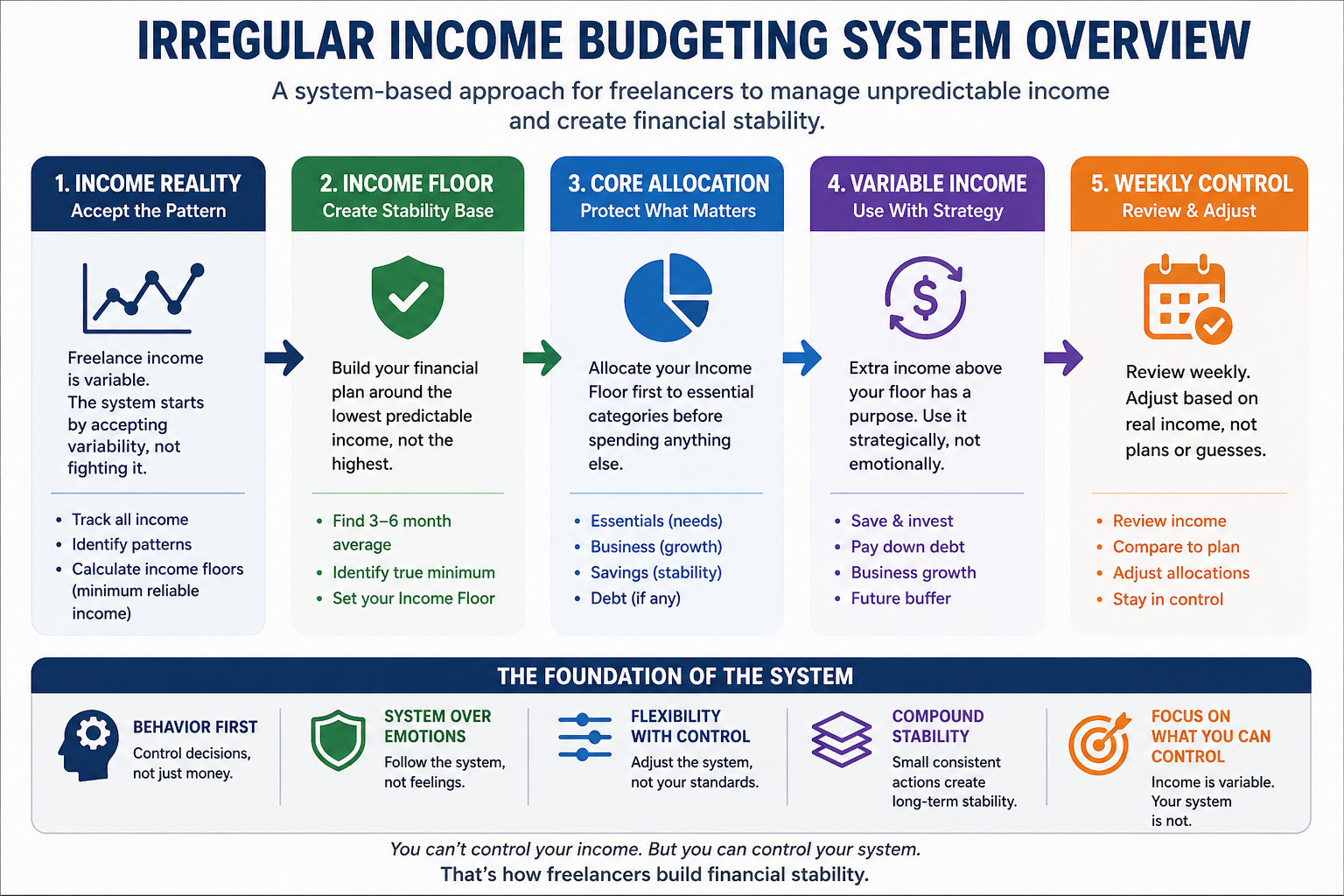

Component 1: Income Floor (Non-Negotiable Stability Layer)

The income floor defines the minimum financial requirement to maintain operational stability.

This includes:

- housing

- food

- insurance

- essential business tools

- minimum debt obligations

This number is not a target.

It is a boundary.

It creates a protected zone where survival is never dependent on future income.

Without an income floor:

- every expense becomes uncertain

- every decision becomes reactive

- financial stress becomes constant

With an income floor:

- decisions stabilize

- uncertainty reduces

- control begins

System Constraint: The income floor must always be secured before any discretionary allocation occurs.

Component 2: Weekly Control Cycle (Volatility Absorption Mechanism)

Monthly budgeting assumes stability across 30-day periods.

Freelance income does not operate in monthly cycles.

It operates in bursts, gaps, and irregular intervals.

The weekly control cycle reduces exposure to uncertainty by shortening decision windows.

This achieves three critical outcomes:

- faster adaptation to income changes

- reduced emotional pressure

- higher consistency in execution

Weekly control aligns financial management with real income behavior.

System Constraint: No financial planning should extend beyond the current control window.

Component 3: Behavioral Allocation System (Decision Alignment Layer)

Traditional budgeting uses categories based on logic.

Freelancers do not operate purely on logic.

They operate under:

- uncertainty

- stress

- income fluctuation

This creates emotional decision-making patterns.

The system replaces rigid categories with behavioral buckets:

- Stability (essentials and fixed obligations)

- Growth (skills, tools, business expansion)

- Future (savings, buffers, investments)

- Joy (controlled discretionary spending)

- Flex (adaptive buffer for unpredictability)

This aligns financial allocation with actual human behavior.

System Constraint: Allocation must follow behavioral structure, not fixed category percentages.

Component 4: Cashflow Timing Awareness (Reality Alignment Layer)

One of the most critical failures in budgeting is ignoring timing.

Freelancers often treat income as available when it is only earned.

This creates false stability.

The system introduces a critical distinction:

Earned income ≠ accessible income

Allocation decisions must only be made using accessible funds.

This prevents:

- over-allocation

- liquidity gaps

- forced financial stress

System Constraint: No allocation is allowed based on expected or pending income.

Component 5: Automation Layer (Cognitive Load Reduction System)

Freelancers operate under continuous decision pressure.

Every financial decision consumes cognitive bandwidth.

Without automation, decision quality degrades over time.

The system removes repetitive decisions through automation:

- tax transfers

- essential bill payments

- baseline savings movement

This preserves mental capacity for higher-value decisions.

System Constraint: Repeatable financial actions must be automated wherever possible.

Why This System Works When All Budgeting Methods Fail

This system does not rely on stable income.

It does not rely on predictable timing.

It does not rely on consistent behavior.

It works because it controls what can be controlled.

Every budgeting method fails because it attempts to control what cannot be controlled.

This system reverses that logic.

It accepts volatility as a constant.

It builds stability within that volatility.

This is why it works under all conditions:

- high income months

- low income months

- delayed payments

- client instability

It does not depend on the environment improving.

It functions within the environment as it is.

This makes it structurally inevitable for freelancers.

This System vs Every Budgeting Method

| Method | Why It Fails for Irregular Income |

|---|---|

| 50/30/20 Rule | Requires fixed income proportions and stable monthly earnings |

| Zero-Based Budgeting | Depends on predicting total income before allocation |

| Envelope System | Breaks when income timing shifts across periods |

| Budgeting Apps | Track spending but do not control allocation timing |

| Irregular Income System | Operates independently of income timing and stabilizes decisions |

The difference is not efficiency.

The difference is structural compatibility.

All budgeting methods assume stability.

This system assumes volatility.

That is why it dominates.

How This System Operates in Practice

Understanding the components is only the first step.

The next step is understanding how they function together as a system.

This is where control is established.

This is where stability becomes consistent.

To properly budget irregular income freelancers, decisions must be controlled by system rules rather than emotional responses to income changes.

How the Irregular Income Budgeting System Works in Practice

The system is not a static framework.

It is an operating loop that continuously adjusts to income variability.

Instead of predicting what will happen, it responds to what actually happens.

This is what makes it stable.

The system operates through a closed control structure:

Income → System Processing → Allocation → Decision Execution → Feedback → Adjustment

Each stage serves a specific function.

Stage 1: Income Entry

Income enters the system only when it becomes accessible.

This ensures that all decisions are grounded in reality, not expectation.

No forecasting is used.

No assumptions are made.

Stage 2: System Processing

Incoming funds are immediately evaluated against the income floor.

If the floor is not secured, allocation is restricted.

If the floor is secured, controlled distribution begins.

This creates priority-based financial control.

Stage 3: Allocation

Funds are distributed into behavioral buckets.

This step determines how money will behave before decisions are made.

Allocation defines limits.

Limits define control.

Stage 4: Decision Execution

All spending decisions are made within system-defined constraints.

This removes emotional volatility from financial choices.

Decisions are no longer reactive.

They are rule-based.

Stage 5: Feedback + Adjustment

Every new income event updates the system.

Allocation adjusts dynamically.

No reset is required.

The system evolves continuously.

This creates ongoing stability without requiring re-planning.

Decision Flow: How Freelancers Actually Use This System

Understanding the flow is what transforms theory into control.

Standard Decision Flow

Step 1 — Income becomes accessible

Step 2 — Income enters system

Step 3 — Income floor is secured

Step 4 — Remaining funds allocated into behavioral buckets

Step 5 — Weekly control cycle distributes spending capacity

Step 6 — Decisions executed within constraints

Step 7 — Next income recalibrates system

This flow ensures that decisions are never based on uncertainty.

Scenario 1: High-Income Month

A freelancer receives a large payment.

Traditional response:

- increase spending

- assume income stability

- expand lifestyle temporarily

System response:

- secure income floor first

- allocate remaining funds across buckets

- maintain controlled spending limits

The system prevents overexpansion.

Scenario 2: Low-Income Period

Income slows or delays occur.

Traditional response:

- panic-based restriction

- cut essential expenses unpredictably

- delay financial decisions

System response:

- operate within income floor protection

- reduce allocation proportionally

- maintain decision consistency

The system prevents instability.

Scenario 3: Irregular Payment Timing

Multiple payments arrive unevenly.

Traditional response:

- misinterpret surplus

- overspend early

- experience shortfall later

System response:

- allocate based on accessibility

- distribute through weekly cycles

- maintain controlled usage

The system prevents false stability.

Before vs After Using This System

Without System (Traditional Budgeting)

- decisions depend on current bank balance

- spending fluctuates with income spikes

- financial confidence is inconsistent

- budgeting feels restrictive and unreliable

- planning breaks under uncertainty

With System (Irregular Income Control)

- decisions follow predefined structure

- spending remains stable across income cycles

- confidence becomes consistent

- financial control becomes predictable

- planning adapts dynamically

The difference is not income.

The difference is control.

How to Maintain System Stability

- always secure income floor first

- never allocate future income

- maintain weekly control rhythm

- use behavioral buckets consistently

- automate repetitive decisions

Consistency maintains stability.

Stability builds control.

System Boundary: What This System Controls (and What It Does Not)

This system is designed to control:

- allocation decisions

- spending behavior

- financial stability

This system does NOT control:

- income generation

- client acquisition

- pricing strategy

These require separate systems.

Confusing boundaries leads to misuse.

Clarity preserves effectiveness.

System Progression: When to Stay, Move Forward, or Return

Stay in this system if:

- income remains unpredictable

- financial decisions feel reactive

- stability is not yet consistent

Move forward if:

- income visibility improves

- cashflow becomes predictable

- financial control stabilizes

Return if:

- income volatility increases again

- decision instability reappears

- system discipline weakens

This ensures long-term system retention.

Explore the System Components (Deep Dive)

This system is built from multiple interconnected components.

Each component solves a specific part of the irregular income problem.

To fully understand and apply this system, explore the following:

-

Why Budgeting Fails Due to Income Timing

This explains the structural mismatch between income timing and expense cycles.

-

Why Irregular Income Feels Unstable

This explains the psychological and behavioral impact of income volatility.

-

Psychology-Based Budgeting for Freelancers

This explains how behavioral systems improve decision-making under uncertainty.

These sub-clusters expand the system into actionable understanding.

They are not optional.

They reinforce how the system operates at a deeper level.

How to Apply This System in Real Life

This system is not theoretical.

It is designed for daily financial decision-making.

Execution happens through consistent application of system rules.

Step-by-Step Implementation

Step 1 — Define Your Income Floor

Calculate the minimum required to maintain stability.

Step 2 — Separate Income Types

Distinguish between earned income and accessible cash.

Step 3 — Allocate Only Available Funds

Never allocate money that has not been received.

Step 4 — Apply Weekly Control Cycle

Distribute spending capacity in smaller, controlled intervals.

Step 5 — Maintain Behavioral Buckets

Allocate funds based on behavioral purpose, not rigid categories.

Step 6 — Automate Repetitive Decisions

Remove cognitive load from recurring financial actions.

This system operates continuously.

It is not set once and forgotten.

It adapts with every income event.

This is what makes it stable under volatility.

If you want to successfully budget irregular income freelancers, the system must be applied consistently using weekly control and structured allocation.

Where This System Fits in FM Mastery

This system is part of the core financial control layer within:

It establishes stability before moving into optimization systems.

Once this system is applied, the next step is:

Cashflow Management for Freelancers

This progression ensures structured financial growth.

Research and Financial Context

This system is informed by research in behavioral finance, income volatility, and decision-making under uncertainty.

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve Economic Data (FRED)

- Deloitte Workforce and Freelance Economy Research

These sources highlight the increasing prevalence of irregular income and its impact on financial decision-making.

This system translates those insights into practical application.

Budgeting With Irregular Income: Key Takeaways

Budgeting with irregular income requires a system-based approach.

Freelancers cannot rely on traditional budgeting methods designed for stable salaries.

Instead, they must:

- build an income floor for stability

- use weekly budgeting cycles instead of monthly plans

- allocate based on behavior, not rigid categories

- manage cashflow timing actively

- use systems to control decisions instead of relying on discipline

This is the difference between temporary control and long-term financial stability.

To budget irregular income freelancers, freelancers must adopt systems that align with income variability instead of fixed monthly budgeting methods.

Definition: Budgeting With Irregular Income for Freelancers

Budgeting with irregular income for freelancers is not a traditional monthly planning method. It is a system-based financial control approach that stabilizes spending, saving, and decision-making by aligning financial behavior with income volatility, timing uncertainty, and behavioral patterns.

Unlike traditional budgeting, which depends on predictable income cycles, this system operates independently of when income arrives. It uses structured allocation, income floors, weekly control cycles, and behavioral buckets to maintain stability regardless of fluctuations in earnings.

This definition reframes budgeting from a planning tool into a decision control system designed specifically for freelancers and independent professionals.

Frequently Asked Questions About Budgeting With Irregular Income

Can freelancers use traditional budgeting methods?

Freelancers can attempt to use traditional budgeting, but it will repeatedly fail due to income timing mismatch. Traditional budgeting assumes stable monthly income, while freelance income is variable and unpredictable.

What is the best way to budget with irregular income?

The most effective approach is a system-based method that includes an income floor, weekly control cycles, behavioral allocation, and timing-aware cashflow management. This ensures decisions remain stable regardless of income fluctuations.

Do budgeting apps solve irregular income problems?

No. Budgeting apps track spending but do not fix structural issues like income timing and volatility. They can support execution, but they cannot replace a system designed for irregular income.

How do freelancers stay consistent with budgeting?

Consistency comes from system structure, not discipline. By using weekly control cycles, predefined allocation rules, and automation, freelancers reduce decision fatigue and maintain stable financial behavior over time.

Why does budgeting feel restrictive for freelancers?

Budgeting feels restrictive because it conflicts with income unpredictability. When a system does not match financial reality, it creates pressure and resistance. A system-based approach removes this friction by aligning with how income actually behaves.

How do you budget irregular income freelancers effectively?

To budget irregular income freelancers, you need a system that uses income floors, weekly control cycles, and behavioral allocation instead of monthly budgeting.

Stop Budgeting. Start Building Financial Control.

Budgeting will continue to fail as long as income remains irregular.

The problem is not discipline.

The problem is system mismatch.

This page has defined the system that replaces budgeting.

The next step is not to learn more.

The next step is to apply it.

Start with:

- defining your income floor

- implementing weekly control

- structuring behavioral allocation

That is where financial stability begins.

👉 Continue here: Cashflow Management for Freelancers